Careful Spending: How students handle credit card debt

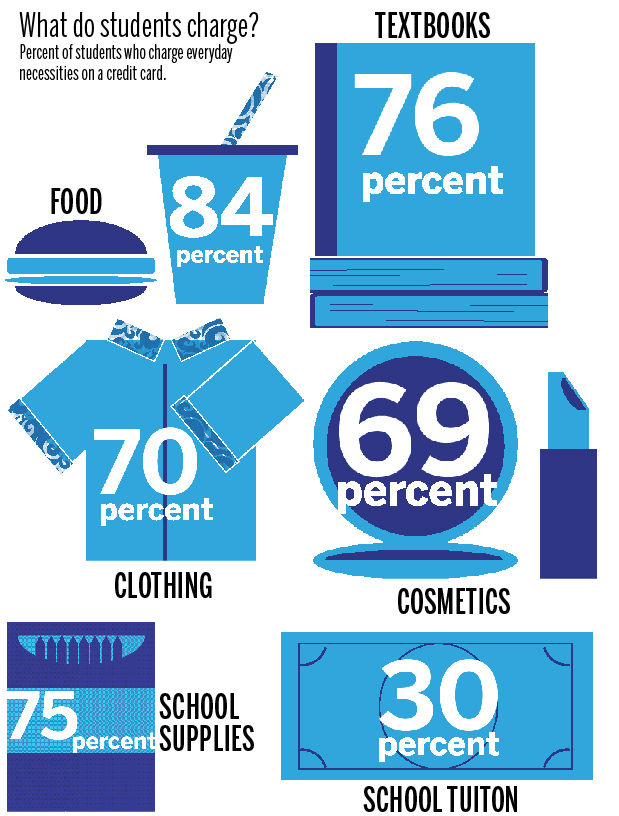

spending graphic fix

September 20, 2015

Credit cards have become nearly unavoidable, and it isn’t uncommon for college students to have at least one credit card, if not more, that they use on a daily basis. What starts as small purchases can quickly add up if not managed properly.

In 2013, the average credit card balance for college students ranged from $136 to $500, according to loan provider Sallie Mae. Add those numbers with high interest rates and a $200 balance that seems like no big deal can quickly spiral out of control.

Northern Ohio Retail Market Manager for PNC Bank, Drew Martin, knows all too well the troubles credit cards can lead to.

“Credit cards can be a major source of financial hardships for anybody, but especially for students,” Martin said. “It’s a whole different kind of financial hardship, you’re responsible for paying that debt as soon as it’s charged.”

Credit cards do pose a lot of risk. But there are ways to avoid trouble and long-term debt: A tip Martin suggested to avoid problems included only having one card, and using it only for emergencies or necessary online purchases. He suggests daily purchases be made with either cash, check or a debit card.

Another tip Martin suggested to students was to read and review their statement every month to see what is spent in different categories like food, clothing and gas. Reading statements regularly will also help students recognize any suspicious or fraudulent charges.

“By keeping track of spending, students can see if they’re getting out of their budget in certain areas,” Martin said. “It helps keep their spending in check.”

Sophomore recreation park and tourism management major Hannah Deascentis uses her credit card for everyday things, but still keeps a careful eye on her purchases.

“I mostly use my card for food and online shopping, like Amazon, but I’m pretty careful,” Deascentis said.

Credit cards do pose a lot of risk to unsuspecting students. But if used responsibly, they can be beneficial in the long run. Maintaining good credit now can help with qualifying for a loan to get a house or a car 10 years down the road.

“We want students to be able to buy a car or their first home and not have to deal with the financial burden caused by credit cards,” Martin said. “If you can eat, drink or wear an item it is probably not a good use of credit.”

Maggie Wachtel is the finance beat reporter for The Kent Stater. Contact her at [email protected].